Introduction

Cost Assumptions and

Simulation-Based Analysis

Scenario 1 (Blue hydrogen production in Korea)

Scenario 2 (Blue hydrogen production in Canada)

Cost analysis of each Scenario using Monte Carlo simulation

Results and Discussion

Conclusion

Introduction

Hydrogen has appeared as an important energy carrier in the energy transition toward sustainable energy systems and plays an important role in decarbonizing multiple sectors including transportation (fuel cell vehicles), industry (ammonia production and refining), and power generation (energy storage and grid balancing) (IEA, 2024). In 2019, the Korean government prioritized hydrogen cars over electric vehicles for economic growth, allocating more R&D funding to hydrogen cars (The Korea Times, 2024). The government announced a roadmap for a hydrogen economy, aiming to create an industry ecosystem covering energy production, storage, transportation, safety, and use in mobility. This initiative is projected to generate 43 trillion Won (approx. 32.25 billion USD) and 420,000 jobs by 2040 (MOTIE, 2019). Public and private sectors are encouraged to cooperate in international technology across the hydrogen value chain.

Various forms of hydrogen are gaining attention for their potential to reduce greenhouse gas (GHG) emissions and mitigate climate change. Gray hydrogen, produced from fossil fuels through processes like steam methane reforming (SMR), releases carbon dioxide as a byproduct, contributing to GHG emissions. Blue hydrogen uses CCS technology to capture and store carbon dioxide during production, making it a lower-emission alternative. Green hydrogen, produced through renewable energy-powered electrolysis, offers a zero-emission solution but faces high production costs and limited infrastructure development (IEA, 2024; Lee and Saygin, 2023). By contrast, blue hydrogen leverages existing SMR and natural gas infrastructure, offering a cost-effective and easy-to-grow solution for the near future (IEA, 2024). Currently, hydrogen production technologies include 48% natural gas reforming, 30% petroleum gas reforming, 18% coal reforming, and only 4% from water electrolysis (KOGAS, 2024).

Blue hydrogen can be produced through SMR, partial oxidation (POX), or autothermal reforming. Among these, SMR is the most commercially prominent method (KEEI, 2023). In SMR, natural gas (methane, CH4) reacts with steam (H2O) at high temperatures (700–1,000℃) in the presence of a catalyst, producing hydrogen (H2) and carbon monoxide (CO):

The hydrogen is purified through pressure swing adsorption and distributed via pipelines or transport carriers. CO2 is separated, compressed, and stored using CCS technologies.

Blue hydrogen emits less greenhouse gases because CO2 generated during production is handled using CCS technology. Continued development of CCS technology is expected to increase its technological maturity, making blue hydrogen the most suitable method for hydrogen production in the mid-to-long term (Hyundai Motor Group, 2022). As CCS technology has advanced, CO2 capture costs have decreased, making blue hydrogen more cost-competitive than green hydrogen in terms of production cost (KEEI, 2023). Furthermore, when the cost of purchasing carbon credits is added to gray hydrogen’s production cost, blue hydrogen production is analysed to be more economical than gray hydrogen production (MSIT, 2024).

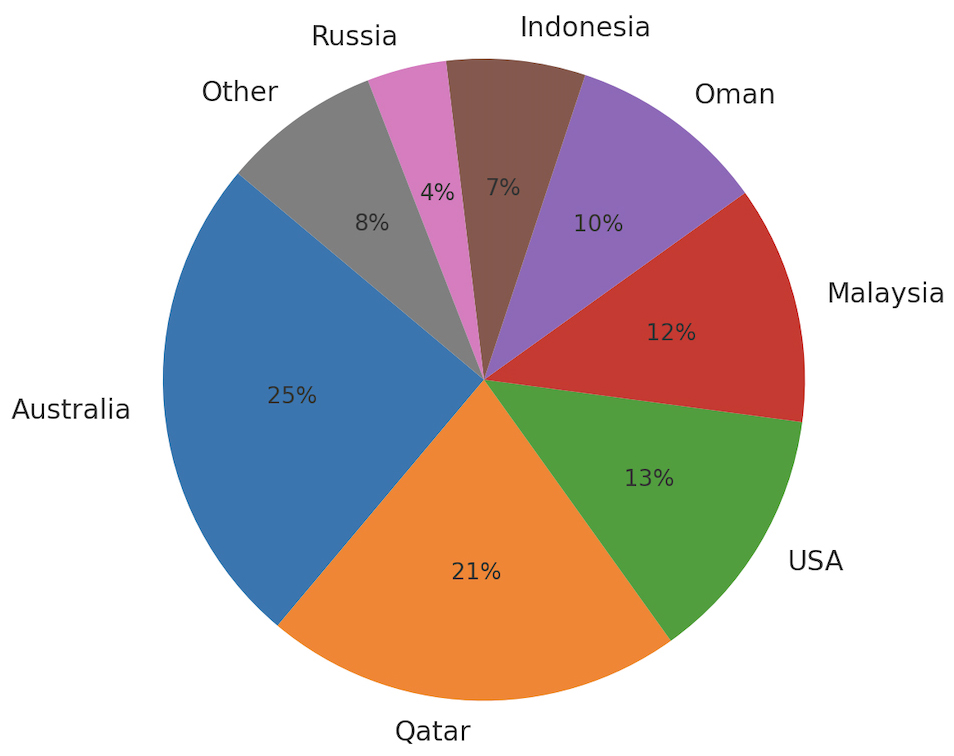

As part of Korea’s hydrogen roadmap, natural gas is the primary feedstock for blue hydrogen. However, Korea relies heavily on liquefied natural gas (LNG) imports from Australia, Qatar, the USA, Malaysia, and others (Fig. 1). Recent energy policy shifts suggest that Canadian LNG may play an increasing role in Korea’s supply mix (MOTIE, 2024). Currently, there is no specific Canadian natural gas exporter to South Korea. However, Canada’s western LNG export projects, such as LNG Canada in Kitimat, British Columbia, are strategically positioned to supply Asian markets, including South Korea. These projects benefit from shorter shipping distances compared to U.S. Gulf Coast terminals, potentially reducing transportation costs and emissions (Natural Resources Canada, 2024). Although current import volumes from Canada are low, Canada's abundant natural gas reserves present an opportunity for future collaboration (CER, 2024). This study evaluates whether sourcing LNG or blue hydrogen directly from Canada can serve as a possible supply pathway. Blue hydrogen is economically and environmentally advantageous relative to gray and green hydrogen. Nonetheless, Korea has limited domestic CO2 storage capacity (The Korea Times, 2024), suggesting that overseas CCS integration or international transport partnerships may be necessary.

Although hydrogen is gaining global attention, there are limited studies that provide a detailed analysis of the Canada-Korea blue hydrogen supply chain, particularly in terms of cost, infrastructure compatibility, and CO2 transport. Korea’s limited CO2 geological storage options and the role of overseas CCS, particularly in Canada, are often overlooked. Bilateral hydrogen trade rules and CCS cooperation are still not fully explored. These rooms show the need for focused research to support practical international hydrogen partnerships. Given the challenges and opportunities, this study evaluates the supply cost of two alternative scenarios for integrating Canadian blue hydrogen into the Korean market. One assumes domestic production using imported LNG and local CCS and the other assumes direct import of processed blue hydrogen in various chemical carrier forms. Using updated data and probabilistic analysis, this study aims to identify the most cost-effective and feasible pathway for supporting Korea’s hydrogen economy goals.

Cost Assumptions and Simulation-Based Analysis

South Korea lacks domestic natural gas reserves and is therefore reliant on imported natural gas primarily in the form of LNG to produce blue hydrogen. This import-dependency has driven the nation’s hydrogen strategy to prioritise energy diversification and the reduction of GHG emissions. Government policies emphasise international cooperation to accelerate technological placement across the hydrogen value chain, particularly highlighting the need for cross-border partnerships in hydrogen production and carbon management. Due to geological limitations, South Korea’s capacity for domestic carbon capture and storage remains constrained, reinforcing the necessity for international collaboration in large-scale hydrogen and CCS infrastructure. Canada emerges as a promising partner in this study, offering abundant natural gas resources, a growing CCS infrastructure, and proximity via its west coast LNG export terminals. The Kitimat LNG terminal in British Columbia was selected for this study due to its strategic location, reduced shipping distance compared to U.S. Gulf Coast terminals, and mature infrastructure (Natural Resources Canada, 2024; LNG Canada, 2024; CER, 2024). A Canada-Korea hydrogen collaboration could offer South Korea access to a stable, low-carbon energy source, while supporting Canada’s ambition to become a global hydrogen exporter.

While this study focuses on the Canada-Korea blue hydrogen supply chain, it is viewed that recent research on Australia-Korea ammonia-based blue hydrogen imports indicates a lower unit cost of approximately 6.3 $/kgH2 followed by liquefied H2 at 12.4 $/kgH2 and liquid organic hydrogen carrier at 13.8 $/kgH2 based on the case of ‘Blue Hydrogen Production in Australia’(Cho et al., 2024). Australia’s well-established ammonia export infrastructure explains its cost advantage. In contrast, Canada is still developing its CCS and hydrogen carrier systems, which results in greater cost variability and technological uncertainty. This comparison highlights the trade-offs faced by hydrogen importing countries like South Korea to strategically choose between established infrastructure and supply chains of Australia and emerging high potential supplier with growing CCS capabilities like Canada (Mishra et al., 2024).

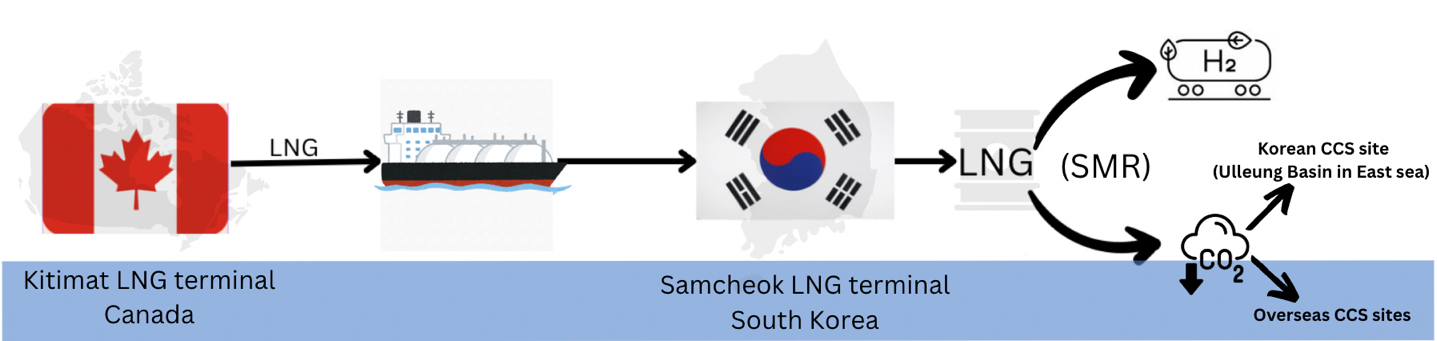

As of 2023, South Korea has seven LNG import terminals in operation, with KOGAS, the state-owned company operating five of them in Pyeongtaek, Incheon, Tongyeong, Samcheok, and Jeju (Fig. 2), while POSCO owns one in Gwangyang and a joint venture between GS Energy and SK E&S operates the Boryeong terminal. These terminals play a significant role in enabling hydrogen production when LNG is imported. The Samcheok terminal in Korea was selected for its advanced LNG handling capabilities (e.g. regasification facilities, sufficient space for expansion) and proximity to regions with high hydrogen demand (KOGAS, 2024). Although Incheon and Pyeongtaek have higher existing hydrogen demand, these locations face space limitations due to urban development and busy LNG operations, making Samcheok a more feasible option for hydrogen facilities. Additionally, Samcheok’s proximity to the East Sea depleted gas field, a promising CO2 storage site, makes it well-suited for CCS integration.

Based on various circumstances including production, transportation, storage, and reconversion costs, two scenarios were designed to calculate the blue hydrogen supply cost from Canada to Korea. The unit cost in this study was adjusted for economic trends and inflation based on 2024 market conditions, converted to the modified cost of each component, and normalized to USD values ($/kgH2) for comparative evaluation. This cost adjustment accounts for economic factors such as production, liquefaction, shipping, storage, reconversion, as well as inflation rates, to reflect real-world volatility and improve reliability.

Scenario 1 (Blue hydrogen production in Korea)

In this scenario, LNG is imported from Kitimat (approx. 7,600 km) to Samcheok, where it is regasified and hydrogen is produced in Korean facilities (Fig. 3). The CO2 captured during the production can be stored in Korean CCS site or exported for overseas storage. The two scenarios in CCS are assumed because CO2 storage capacity is relatively limited in Korea. However, overseas CCS (Canada) option was excluded from this study due to limited data availability, uncertainty in the international regulatory framework, and the absence of a defined cost structure for cross-border CO2 transport and storage. In Korea, the depleted East-1 gas field can store only 1.2 million tons of CO2 annually (KNOC, 2024). This planned capacity is insufficient to accommodate approximately 5.2 million tons of CO2 generated annually from domestic H2 production (EG-TIPS, 2024). Therefore, overseas CCS storage sites should also be considered. Among potential domestic CO2 storage sites in West Sea, South Sea and East Sea, the Ulleung Basin in East Sea is the only site evaluated as suitable in terms of both scale and geological characteristics. For this study, only domestic CCS storage was considered, with a CO2 sequestration cost of 0.15 $/kgH2 (IEA, 2019). The cost structure includes LNG production at 1.47 $/kgH2 (Canadian Energy Centre, 2024), ocean transport at 4.40 $/kgH2 (Al Ghafri et al., 2023), regasification at 2.96 $/kgH2, and hydrogen production and CO2 capture at 5.56 $/kgH2 (GIST, 2018).

Table 1 summarizes the cost components including LNG production in Canada, shipping to Samcheok, LNG regasification, domestic hydrogen production via SMR, and domestic CCS storage.

Table 1.

Implementing unit cost for Scenario 1

| Location | Cost | Unit | Mean | Variance | Reference |

| Canada | LNG production | $/kgH2 | 1.47 | 0.05 | Canadian Energy Centre (2024) |

| Ocean | LNG transportation | $/kgH2 | 4.40 | 0.15 | Al Ghafri et al. (2023) |

| Korea | LNG regasification | $/kgH2 | 2.96 | 0.10 | GIST (2018) |

| H2 production (SMR) | $/kgH2 | 4.82 | 0.12 | GIST (2018) | |

| CO2 capture | $/kgH2 | 0.74 | 0.03 | GIST (2018) | |

| CO2 sequestration | $/kgH2 | 0.15 | 0.01 | IEA (2019) |

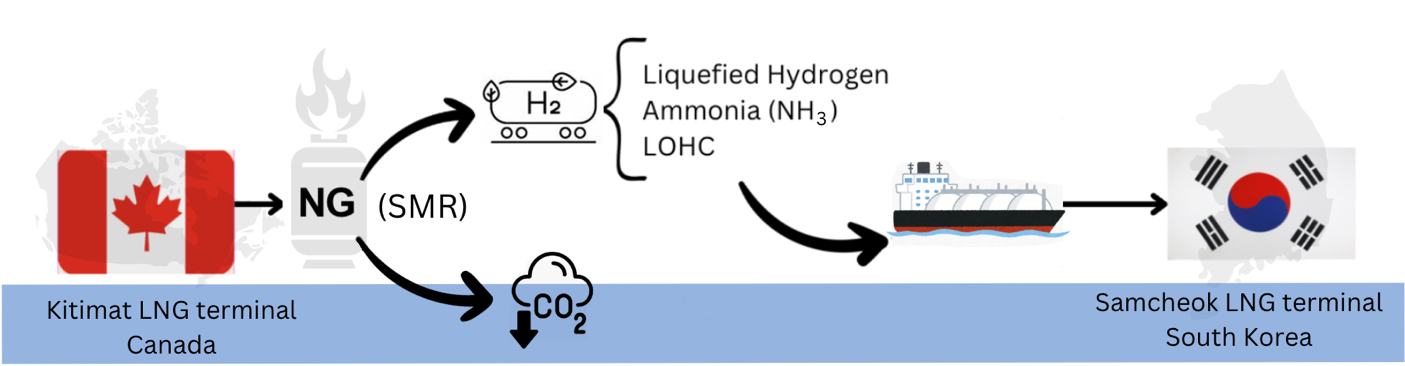

Scenario 2 (Blue hydrogen production in Canada)

In this scenario, blue hydrogen is produced in Canada and can be imported to Korea via liquefied hydrogen (LH2), ammonia (NH3), or liquid organic hydrogen carrier (LOHC) as shown in Fig. 4. Hydrogen production with CCS is estimated at 1.20 $/kgH2 (Layzell et al., 2020). LH2 is cooled to –253°C for transport, while ammonia and LOHC carry hydrogen by chemically binding it within their molecular structures. Therefore, hydrogen storage costs vary by carrier, and the import unit cost is calculated separately. The storage costs are follows: LH2 (4.57 $/kgH2), NH3 (2.83 $/kg H2), and LOHC (4.50 $/kgH2) (BloombergNEF, 2020). Transport costs are 2.85, 2.05, and 2.25 $/kgH2, respectively (IEA, 2023). Reconversion costs are 5.50 for LH2, 1.25 for NH3, and 4.95 $/kgH2 for LOHC (Raab et al., 2021; Hydrogen Council, 2021; European Commission, 2018).

Cost data reflects publicly available benchmarks and regional market values. The ammonia pathway in the Scenario 2 offers the lowest total cost at 7.33 $/kgH2, comparing to LH2 and LOHC which is 14.15 $/kgH2 and 13.7 $/kgH2.

Table 2 includes Canadian hydrogen production with CCS, blue hydrogen production, shipping to Korea and reconversion. Each cost reflects the adjusted unit cost based on recent market fluctuations for consistency.

Table 2.

Implementing unit cost for Scenario 2

| Location | Cost | Unit | Mean | Variance | Reference |

| Canada | H2 production with CCS | $/kgH2 | 1.20 | 0.05 | Layzell et al. (2020) |

| H2 storage cost | |||||

| - Liquid H2 | $/kgH2 | 4.57 | 0.10 | BloombergNEF (2020) | |

| - Ammonia | $/kgH2 | 2.83 | 0.08 | BloombergNEF (2020) | |

| - LOHC | $/kgH2 | 4.50 | 0.09 | BloombergNEF (2020) | |

| Ocean | H2 transportation | ||||

| - Liquid H2 | $/kgH2 | 2.85 | 0.12 | IEA (2023) | |

| - Ammonia | $/kgH2 | 2.05 | 0.10 | IEA (2023) | |

| - LOHC | $/kgH2 | 2.25 | 0.11 | IEA (2023) | |

| Korea | H2 reconversion | ||||

| - Liquid H2 | $/kgH2 | 5.50 | 0.15 | Raab et al. (2021) | |

| - Ammonia | $/kgH2 | 1.25 | 0.07 | Hydrogen Council (2021) | |

| - LOHC | $/kgH2 | 4.95 | 0.14 | European Commission (2018) | |

Cost analysis of each Scenario using Monte Carlo simulation

Monte Carlo simulation was employed to calculate the hydrogen implementation costs, given that scenario-specific cost components are influenced by technology maturity and process efficiency. Each cost component was modeled with a normal distribution to capture variability associated with technological advancement and market fluctuations (Khindanova, 2013). The simulation was run 1,000 times using random sampling, and resulting hydrogen implementation cost outputs were averaged to evaluate the economic feasibility of each scenario, providing more estimates of mean and variance (Cho et al., 2024). Where data was unavailable, estimates were informed by market unpredictability and expert judgment- for example, in the variability of LNG transport and reconversion costs.

Results and Discussion

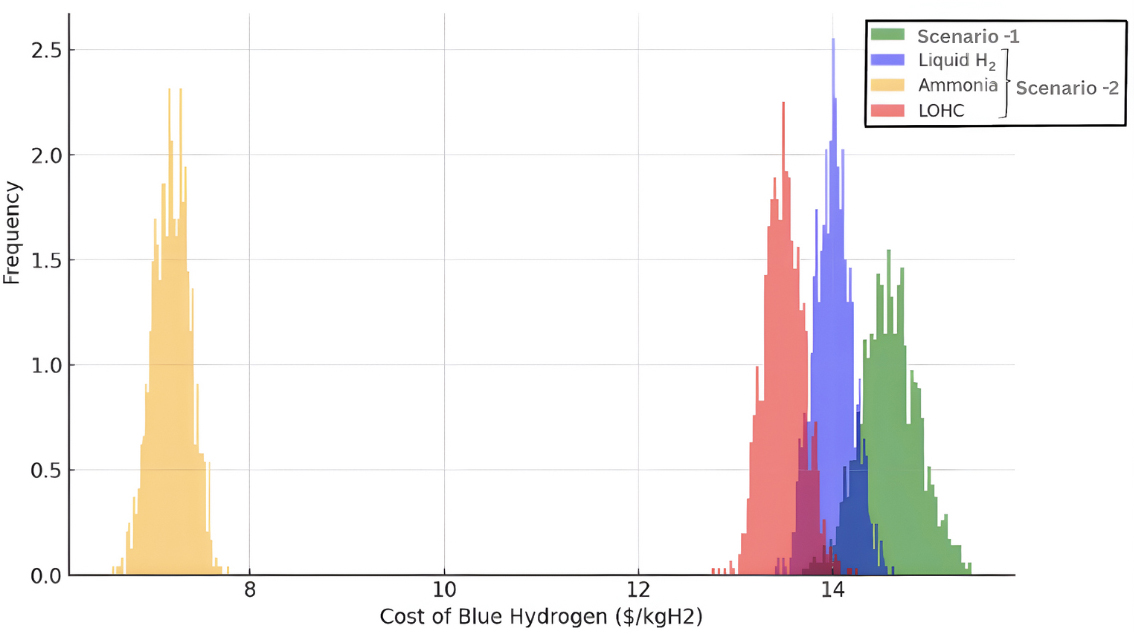

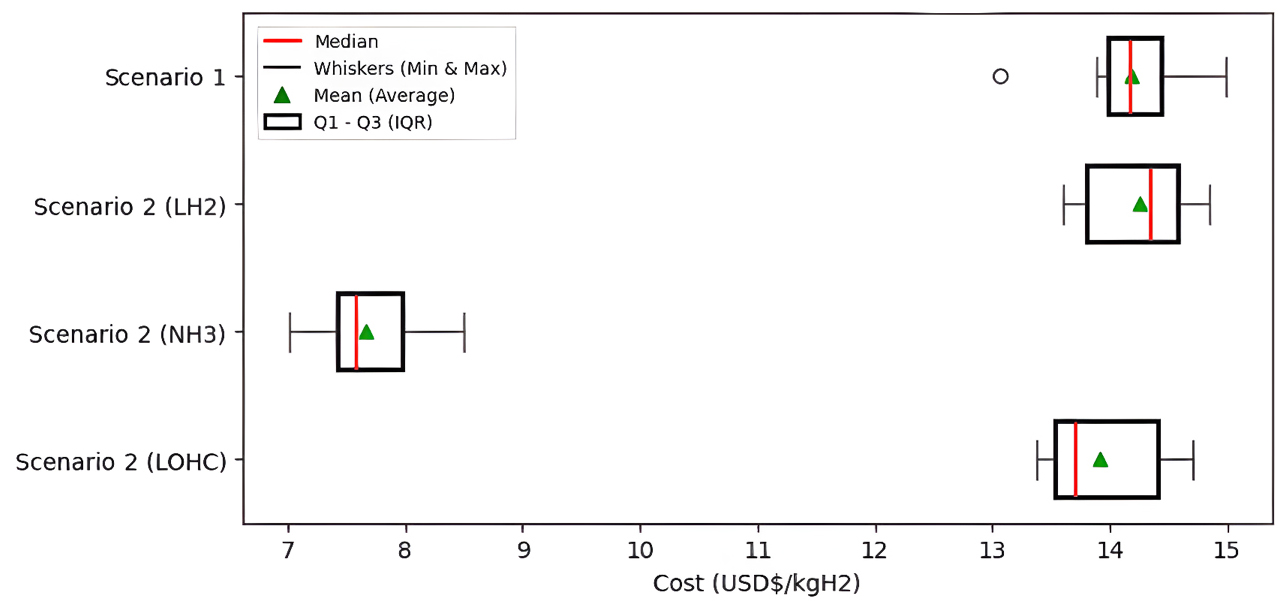

The Monte Carlo simulation results show a clear difference in cost and economic feasibility across the scenarios. In Scenario 1, the average cost of producing blue hydrogen domestically by importing LNG is estimated at 14.57 $/kgH2, with a variance of 0.48. This high cost -compared to other scenario- is attributed to increased expenses related to LNG production, long-distance maritime transport, regasification, hydrogen production via SMR, and CO2 capture and sequestration within Korea. Table 3 summarizes the final cost and variance of hydrogen supply for each scenario. Scenario 2, which involves the direct import of blue hydrogen from Canada to Korea, presents an average cost for each hydrogen carrier: LH2 at 14.15 $/kgH2 with a variance of 0.45, NH3 at 7.33 $/kgH2 with a variance of 0.13 and LOHC at 13.7 $/ kgH2 with a variance of 0.19. These results are consistent with previous research (Cho et al., 2024), indicating that importing hydrogen as ammonia is the most economical and stable option due to its lower conversion and reconversion costs and well-established export infrastructure.

Table 3.

Final H2 implementation unit cost analysis

| Cost ($/kgH2) | Variance | |

| Scenario 1 | 14.57 | 0.48 |

| Scenario 2 | LH2: 14.15 | 0.45 |

| NH3: 7.33 | 0.13 | |

| LOHC: 13.7 | 0.19 |

Fig. 5 shows the cost distributions for simulated blue hydrogen cost in Scenario 1 and Scenario 2. A comparison of implementation costs reveals a significant variation influenced by H2 production location, storage method, and CCS storage site. Fig. 6 compares supply costs across all scenarios, showing that importing LNG from Canada for domestic hydrogen producing in Korea is the most expensive option. In contrast, ammonia presents the lowest cost pathway. While LH2 and LOHC are somewhat less expensive than domestic production, their costs remain higher and more volatile than those associated with ammonia.

While Korea is actively developing CCS infrastructure (e.g., the depleted gas field in the East Sea), the current limitations in domestic CO2 storage capacity (1.2 MtCO2/year at the East Sea site; KNOC, 2024) and technology readiness result in higher costs and uncertainty for Scenario 1. This necessitates either reduced CO2 emission volumes or future partnerships for overseas CO2 sequestration. Thus, Scenario 2, particularly utilizing ammonia as the storage carrier, emerges as the most feasible and cost-effective strategy for blue hydrogen supply.

These findings align with global assessments by the IEA (2023), Hydrogen Council (2023), and Lee and Saygin (2023), all of which emphasize ammonia’s cost-effectiveness and scalability for hydrogen transport. Moreover, this study provides an economic assessment of a cross-border blue hydrogen supply chain, incorporating detailed cost analysis, transportation pathways, and CCS scenarios. This study will contribute to strategic decision-making by comparing hydrogen supply options and evaluating their feasibility within the context of Korea's energy transition goals. However, the analysis is limited by assumptions on future market prices, technological maturity, and evolving regulatory frameworks. Environmental and social impacts were not deeply explored. Future research could extend to life cycle emissions analysis, integrate dynamic market modelling, and examine public acceptance of hydrogen technologies across different regions.

Conclusion

This study evaluated two blue hydrogen supply scenarios between Canada and Korea using cost modelling and Monte Carlo simulation. In Scenario 1, LNG is imported and hydrogen is produced domestically in Korea via SMR with CCS, yielding a high average cost of 14.57 $/kgH2. In contrast, Scenario 2 involves producing hydrogen in Canada and importing it in carrier forms, demonstrating more favourable economics. The estimated hydrogen implementation cost is 7.33 $/kgH2 for ammonia (NH3)-lowest and most stable- 14.15 $/kgH2 for LH2, and 13.7 $/kgH2 for LOHC.

Among the options analysed, ammonia is the most cost-effective hydrogen carrier for supply from Canada to South Korea. This outcome likely stems from its established infrastructure, lower transportation and reconversion costs, and global recognition as a viable hydrogen carrier. Ammonia can be stored and transport hydrogen efficiently over long distances. Although future advancements in CCS technology and domestic infrastructure may improve the feasibility of Scenario 1, current limitations and higher cost variability make importing blue hydrogen in the form of ammonia (Scenario 2) a more viable option. This strategy not only offers economic advantages but also aligns with Korea’s hydrogen roadmap, supporting long-term goals for decarbonization and energy security.